For many, founding a startup is a dream come true and it should. It’s about controlling our own destiny, making an economic impact, solving problems, building wealth, and making a difference in the world we live in. Sounds magical? Let’s change the last statement into a series of questions: how can we control our own destiny, make an economic impact, solve problems, build wealth, and make a difference in the world we live in? Time for some key startup lessons every entrepreneur must learn.

If it was as easy as dreaming, Google searching, Facebook advertising, logo design, app development, and a featured article, every rational person would have no plans but to build startups, that is, there will be more entrepreneurs than employees, new markets will emerge, existing ones will saturate, and the economy will be disrupted possibly to the best or the worst. There is one fact that is stopping this from happening; entrepreneurship is not for everyone.

Do we all choose uncertainty over security? Risky success over roadmap to success? Imbalance over balance? Two birds in the bush over one in the hand? Most of us don’t despite the fact that many full-time jobs are as stressful, if not more stressful than building, running and growing startups. For those who do, here are 46 very important startup lessons you must learn.

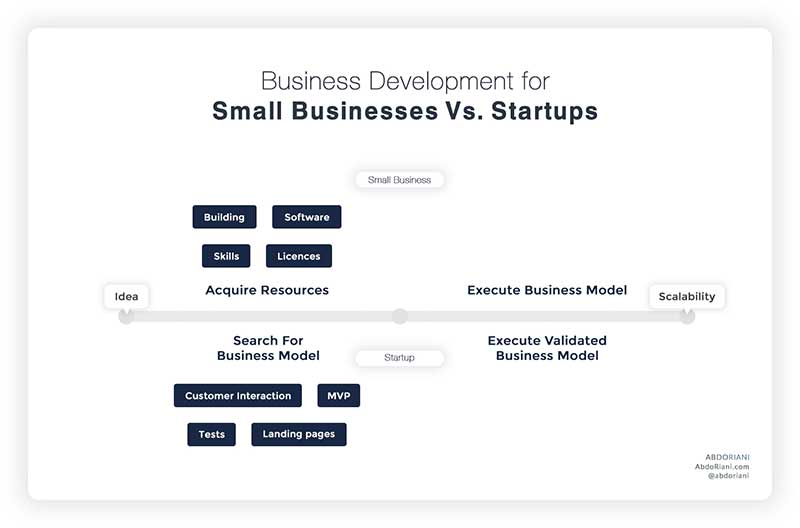

Startup Lessons 1: A Startup Is Not A Small Business

It is a phase and not a type of business. It is the phase during which founders aim at finding and validating a model that scales repeatedly, usually by leveraging technology. Startups are built for growth and it is for this main reason that most startups are tech startups; reaching more people through technology. Small businesses, in the other hand, execute proven models rather than search for one such as owning a restaurant, barbershop or a grocery store. From a business and revenue model perspective, small businesses are ahead of the curve.

- A CPA office is a small business whereas a software that matches clients with local CPAs is a startup.

- A taxi company is a small business whereas a software that matches riders with nearby taxis is a startup.

- A social media studio is a small business whereas a software that plans and automates social media sharing is a startup.

- A magazine is a small business whereas a software that enables users to create their online magazines is a startup.

- A web development company is a small business whereas a software that enables users to create their own software is a startup.

Notice how technology triggers scalability and reach. It is the uncertainty in business model validation (among others) that makes startups riskier. In other words, are we certain that people want to be matched with local CPAs? That people prefer the convenience of a software over a social media manager? That people want to use an app to book rides? Who specifically out of everyone prefers those services? etc. Startups must find valid answers to these questions before reaching a sustainable business. In the meanwhile, according to the small business administration and a Startup Genome report, 92% of startups fail within the first 3 years while only 32% of small businesses do.

Startup Lessons 2: It’s Not Just For High School And College Kids

And here’s the proof: according to a Harvard study,

- The average founding team is aged 35 to 44.

- Companies with an average age of 26 to 34 have the highest median funding.

- Of startup founders, less than 1% start before the age of 20, 34% start between the ages of 20-29, 40% between the ages 30-39, 20% between 40-49, and 5% over 50 years old.

- Of startup founders, 39% were previously CEOs/founders, 28% entry to mid-level employees, 10% directors, 9% VPs, 5% Sr. VPs, 5% managers, and 5% consultants.

- Of startup founders, 70% are married when they start their first startup venture and 60% have at least one child.

The narrative many of us are familiar with about the college dropout dreaming of building the next hundred billion dollar company is glamorous for a Hollywood movie but certainly not the norm in real life.

Startup Lessons 3: Failure Is Part Of The Startup Success Formula

This essentially applies to anything in life but we have numbers to back this statement when it comes to building startups. According to a research study by Paul Gompers, Josh Lerner and David S. Sharfstein, first time entrepreneurs have an 18% chance of succeeding (from idea to exit) with their ventures whereas those who failed once have a 20% chance of making it the second time.

Furthermore, with a successful startup in the books, founders have a 30% chance to build another successful venture. That is, startup founders are more likely to build a successful company if they failed than if they’ve never tried. Don’t be afraid to fail; it’s all part of the startup success formula.

Startup Lessons 4: Startups Maily Fail Because of Lack of Market Need

Remember the distinction between startups and small businesses above? CB Insights found that 42% of startups fail due to lack of market need for their products. Back to our examples, startups fail mostly because they find that people don’t really need a software that matches them with local CPAs, or the convenience of a software over social media managers, or an app to book rides.

Most startups fail because they build products not enough people need. Entrepreneurs’ main responsibility and concern should thus be in validating the need for their solution before wasting time building great products that people won’t pay for or use at all.

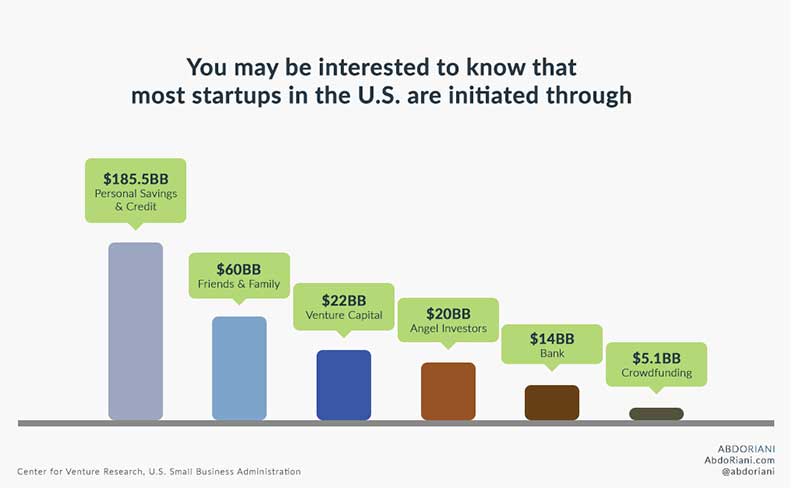

Startup Lessons 5: Most Startups Are Self-Funded

According to Fundable, less than one percent of startups are funded by angel and venture capital investors. 0.05% of startups receive venture capital funding while 0.91% are angel funded. Building or at least initiating a startup venture using personal savings, credits, family and friends has been the medium for most startup founders. 80% of startups are self-funded.

Furthermore, it has been increasingly challenging to secure funding among the pool of startups that emerge on a weekly basis which is setting the standards for funding higher and higher where funding ideas becoming obsolete. In sum, funding for growth is essential and will be inevitable once founders build enough value through hustle and a little bit of self-funding.

Startup Lessons 6: Money Helps But Not Essential To Start A Startup

From idea to initial traction, the steps taken by founders of venture capital/angel funded and personal funded startups is the same. That is, startups with half a million dollars in funding will take the same route as those with $5,000 in the bank. Customer interaction, prototyping, MVP development, quantitative and qualitative testing, etc. are all accomplished through one to one meetings, online surveys, wireframing and prototyping platforms, app development platforms and freelancers or team members, google analytics, etc.

Depending on the model, concept, industry and whether the product is a hardware or software, the steps that need to be taken and the resources needed to reach a level of validation that justifies aggressive growth is the same. Money is thus not an excuse for failure to initiate and put in the effort to measure, track and evaluate user needs.

Startup Lessons 7: A Startup Is Not An App

Developing a startup app is about one thing: solving a problem. A hardware, web, and/or mobile app are the medium by which problems are solved, also known as product. Startups that focus on perfecting the functionality and look of their products can miss the problem, how it should be solved and who it should be built for. Startups should thus start by defining the problem, proving its existence and need for a solution, proposing and testing multiple solutions, then finally build a great product while keeping in mind that,

Startup Lessons 8: There Is No Such Thing As Bug-Free Software

Especially with complex software. Frequent changes in software specification, architectural decisions, requirement gathering, usability, robustness, etc. are a few reasons why complex software, one that attempts to solve big problems faced by many people at the same time, will have bugs in one way or another. Startups build great products, ones with less bugs and better experience, over time. This is part of the success equation since one of the main reasons behind startup failure is premature scaling, according to the Kauffman Foundation.

Startup Lessons 9: An Idea Is Just A Guess Until Validation

Unless there is a startup for voting the best ideas with an algorithm that quantifies ideas’ worth based on user demand, engagement and bid, ideas are worthless. In other words, an aha moment is nothing but a guess that something might happen if certain conditions are met. Only when such conditions (users willing to pay, register, refer friends, come back, email you with requests, etc.) are met, will there be value in ideas. By then, ideas will no longer be ideas; they will become startups. Execution is therefore the only way founders can build value.

Startup Lessons 10: Culture Matters

It is the set of written and unwritten rules, values, and assumptions by which a startup operates and grows. More often than not, the startup culture takes after the styles, beliefs and personalities of the founders. While there is nothing wrong with that, it can be a limiting factor in startup growth, especially if the startup grows out of the initial startup phase and the values and principles that should drive the startup are not aligned with the culture. For instance, if among the rules and values in the culture of a startup are about taking measurable decisions, minimizing risk, and hiring locals first, growth potential and investors’ interest decline consequently.

Furthermore, startup culture has been shown to have a major impact on recruitment and employee retention. A survey by a commercial real estate startup, TheSquareFoot, revealed that for workers, culture is as important as business strategy, has a major impact on employee happiness and satisfaction, affects financial and employee performance, and highly influenced by the physical office space. Why is this so important? First, the findings show that startups with happy employees outperform the competition by 20% and secondly, highly engaged employees are 38% more likely to have above average productivity. But most importantly, because

Startup Lessons 11: Team Is The Most Valuable Asset In Early Stage Startups

Every innovation is fueled by human capital so there is no doubt that a team is what drives every success story. However, at startups’ initial stages, with just an idea, vision and founders’ passion to build the next big thing, it is the team by which the startup is valued, that is, it is the team that investors fund, accelerators and incubators recruit, and key talents decide to join. Building a startup team with a shared passion, vision and with skills that complement each other should thus be one of the main priorities of entrepreneurs while keeping in mind that,

Startup Lessons 12: If You Don’t Have One, You Don’t Need A Team To Start

Building an A star team is easy said than done especially at a stage when all what the founders own is practically nothing unless vision, passion and willingness can be quantified. The best founding teams are built years before the beginning of any startup venture. Those are older friends with common interests, shared values and objectives who happen to be ready to turn an idea into a solution that can be used by millions.

What about founders who don’t have such friends? The answer is that most people are not fortunate to skip the hustle of building a founding team so the majority of startup entrepreneurs are searching for their complement as we speak. Searching is not a standalone activity and must take place in parallel to startup building. And this is due to many reasons.

First, team is an essential ingredient for solid startup growth, funding and attracting other key talents, but not necessarily for startup venture initiation, that is, testing user needs, viability of the proposed solution, traction, initial validation, and potentially customer orders. Second, competition for the best co-founders/team members is very high that an idea and a compelling vision is no longer sufficient to grab members’ interest.

Third, searching time can be wasted if the proposed solution eventually turns out to be a failure in addressing user needs and solving the problem in hand. Fourth, regardless of founders’ background (business, marketing, finance, engineering, etc.), there are many free and affordable resources that can be leveraged to make significant progress such as prototyping and wireframing platforms, app builders, theme marketplaces, freelancing sites, etc. Execution is thus the best recruiting marketing channel.

Startup Lessons 13: Don’t Give Away Equity To Strangers

Startup co-founding relationships are often described as marriage for the purpose of growing a baby (idea) into a grown and self-responsible company. We’ve heard about love from first sight but never have we seen marriage from first, second or even third meeting. This is a killing mistake that many first-time entrepreneurs are tempted to make when, after months of searching for the perfect co-founder, they meet an ideal person and offer an equity partnership a lot sooner than needed.

Founders must spend quality time to learn more about potential co-founders and take legal measures to ensure co-founders’ real intentions in building a valuable startup as per the discussions and verbal agreements between each other. Legal measures can take the form of performance based compensation and a testing period through cliff and vesting schedules, this is especially true if the startup is funded at the time of the co-founding agreement.

Startup Lessons 14: No Co-Founder Is Better Than Bad Co-Founder

In a Harvard study, of startups, 39% have one founder, 40% have two, 19% have three, and 4% are startups with 4 co-founders. A co-founder can take a startup to the next level, make a marginal difference or be determinantal. Good co-founders add startup value by bringing complementary skills, new perspectives, energy and commitment. Ineffective co-founders have similar backgrounds, skills and experience as existing member(s) and contribute mainly in brainstorming and hustle.

Detrimental co-founders drag everyone down, drain their energy, divert their strength and kill their dreams. No co-founder is better than mediocre cofounders and certainly better than a bad fit between skilled co-founder candidates and company culture.

Startup Lessons 15: Working Hard Doesn’t Guarantee Success. Working Smart Can.

Startup hustle isn’t about running after every potential buyer, using every sales technique in the book, showing up to every networking event, pitching products in every opportunity there is, cold calling, fighting for featured posts, etc. also known as forcing an undesired and unneeded solution into the hands of customers.

Smart startup grinding is about listening more than doing. It is about seeking potential users’ feedback to learn more about their big problems and urgent needs; it’s about using several techniques to validate the identified problems and needs, and then building a solid product for further validation before any aggressive selling can take place. The hustle for early-stage startups is thus more strategic than physical.

Startup Lessons 16: Your Main Responsibilities Are Not Always What You Specialize In

First of all, there is no such thing as the idea guy; idea generation is not a role.

Complete founding teams usually include a business development and marketing person, designer and programmer. Such combination is not given. Often times, one or two of these key members are missing. Regardless of whether the team includes these assets or not, rarely will members do the things that are only great at. Thus, founding members should expect and embrace their strategic, decision making, programming, recruiting, customer service, sales, cheerleading, marketing, and designing roles among others.

The good news is that the only way members get to do what they enjoy the most, most of the time, is when they take the startup to a level where growth justifies building a bigger team with narrower focus.

Startup Lessons 17: The Numbers Don’t Look Good. But That’s The Point!

Nine out of ten startups will fail. This means one thing: if you make it, you are unique. Better odds of success are not in entrepreneurs’ favor. That will simply mean that many can make it, many will thus attempt to make it, and the pie will thus be sliced too thin that hardly will anyone ever make it too big. There are other economic impacts to easier barriers to entry and success but the moral of the story is that entrepreneurs must embrace the challenge and fight to stand alone for the big prize.

Startup Lessons 18: You Can Start Tomorrow

Not after you finish a book, course, seminar, school, raise money, save money, or during the next break; tomorrow can be the day you start executing on your ideas. All you need is one business lesson: a startup solves a problem via a solution (product) and in exchange, customers will pay (or use it) for it.

As a founder, you have three main responsibilities: prove that a problem indeed exists, the proposed solution solves the problem, and as a consequence customers are willing to pay for it. There is one rule to live by: since revenue is the fuel for every business and since money is paid by customers, only them can identify the three Ps: problem, product and payment. Therefore, as a founder, potential customers should be your mentors, advisors, and investors.

If entrepreneurs are serious about executing on their ideas, nothing can justify delays because meeting with customers for qualitative validation is the first, one of the most important, and continuous steps that every entrepreneur should take. And it does not require an investment, product, or development plans and deadlines.

Startup Lessons 19: You Don’t Always Need A Prototype

A prototype is a functional or visual example of what you envision building. Functional or visual, three are those who you would build a prototype for: potential customers, investors, and/or team members. From a customer stand point, the question is, will potential buyers be sold on the idea when they see how it looks (visual prototype) or do they need to see it working (functional prototype)? Only customers can answer this question.

Will a prototype get you funded? and, is the idea very hard to explain that a prototype will make team brainstorming and decision making easier? The answer to all these questions can be: I use the competition, I looked at your designs, I can see how it will work, I just want to use it. Or, we don’t fund prototypes; we need validation and traction. Or, let’s save some time by sketching on the board. In these cases, you don’t need a prototype.

The right answers always come from end users and not books or mentors. The first series of questions should be asked to a sample from the end prototype users (customers, investors, and team members).

Startup Lessons 20: An MVP Doesn’t Always Need Code

A Minimum Viable Product (MVP) is the version of the product that includes only the necessary (usually core) features to gather quantitative feedback for learning and validation. As stated, MVPs provide quantitative feedback, so do all solutions require code (web or mobile) to quantitatively measure user interaction and behavior? No.

For example, think about an on-demand service say for food, what if we create a Facebook page called Food On Demand, shared it with all our friends, monitored page visits and phone calls, would this give us the quantitative insights we need with only the necessary features we borrowed from Facebook? absolutely; enough information to learn about user needs, intentions and demand. The same logic can be applied to other models and thus MVPs don’t necessarily always need code.

Startup Lessons 21: You Don’t Always Need A Mobile App

There are a few things to consider when deciding to build a web, mobile or both apps. Everything is always centered around end user needs and expectations, meaning that customer interaction is the answer to most questions. But keep in mind that internet users prefer web applications or mobile responsible we apps for shopping, search and entertainment according to a study by MDG. For information (news), navigation (e.g., ride sharing), and social interaction, users are more likely to use mobile. To begin, identify and select users’ desired platform then expand across others upon validation and growth.

Startup Lessons 22: Build One Startup At A Time. Not More Than One At Once

Entrepreneurship works within limits. In other words, it is a combination of many ideas floating around our head and a limit to the reserve of resources we can use to make some of them come true. Building two startups at once is not a risk diversification. As a startup founder, you are in a search mode. You are searching for the right solution (business model) for the identified problem.

Building more than one startup at a time simply means even more uncertainty. And when uncertainty is multiplied, entrepreneurs often select the startup idea they are most passionate about. Therefore, feel free to test multiple ideas at once since You Can Start Tomorrow, but stick with the one that solves the biggest problem, addresses the most urgent need and is a field you have passion for. This startup rule is unlike small businesses where, with enough resources, owners can delegate and evaluate periodically.

Startup Lessons 23: Yes, You Can Make Money Before Building A Product

The Food On Demand example above is a case where founders do not need a product to start generating revenue. Using existing nonscalable resources is the answer to making money before building a product. In other words, it is about simulating the solution using existing ones that may have nothing to do with the product but can be of use to solve the intended problem in a nonscalable way.

For instance, a simulation of an Uber concept can be as simple as a social media page with a phone number for riders to call. One of the team members picks up the phone, learns about the location of the rider, uses Find My Friend app to locate the other team members or contractors, calls the closest person, and confirms with riders.

This simulation of the solution is nonscalable and has a lot of limitations but can save founders a lot of time in development until validation (a lot of people call), generate revenue and possibly use it as a story to tell investors and future app users. Startup founders must consider alternative nonscalable resources to solve the problem before beginning code.

Startup Lessons 24: Freelancers Can Help

The internet revolutionized accessibility. From an entrepreneurship stand point, it is becoming increasingly easy and convenient to access and employ talents in a matter of minutes. Not to promote instant hiring, but the role that freelancers can play in startup development is principle and is in fact becoming essential.

Freelancers can help but should not be the only human capital in the team for many reasons with misalignment of interest being the most important one. In other words, no matter how trustworthy, punctual and responsive freelancers are, they are usually not founding the startup and their involvement ends with employers’ pay.

In the Uber example above, freelancers can turn the nonscalably validated concept into a scalable application if the founder does not have the technical skills to build the app. The involvement of a freelancer in this case enables founders to progress with the startup and build a stronger case to attract investors and co-founders’ interest.

Startup Lessons 25: A Mentor Is An Asset

Research by MicroMentor shows that mentored founders increased their revenue by an average of 106% whereas those are not, experienced a 14% increase only. The same study shows that 49% of potential founders who received mentoring ended up starting their businesses and 82% survived for 1-2 years; 13% higher than the average new business survival rate.

Furthermore, a study by TechCrunch finds that 33% of founders who are mentored by successful entrepreneurs went to become top performers: 3 times more likely to reach an exit of $100 million or be in the top 10% in terms of the amount of equity raised, or in the top 10% in terms of number of employees. Good mentors clearly make tangible impact. Seeking and finding the best mentors is a similar process to finding the best co-founders and investors. It is about nurturing relationships.

Startup Lessons 26: Take Control Of What You Can Control

Choosing how much effort to put in, how much money to spend, who to hire, how fast you want to grow, and which customer segment to focus on are among the things founders can fully control most of the time. Rise of the competition, the amounts they raise, environmental circumstances, technology shifts, and personal crises that impact family and employees are among the things entrepreneurs usually have no control over.

Countless are the startups that managed to fail despite team members’ qualification, their effort and money raised. Startups are better off worrying less about the things they can’t control and more about the things they can.

Startup Lessons 27: Startups’ First Biggest Milestone Is To Find Product-Market Fit

A research study by CBInsights finds that the number one reason (42%) behind startup failure is lack of market need. There is a fit between the product and the market when the proposed solution proves to satisfy the need or solve the problem of a target group. CBInsights’ findings show that most startups fail to find this fit or even a need for a solution in the first place.

Reaching product-market fit can be recognized through signals such as customer acquisition cost going down, demand and revenue grow exponentially (on a weekly basis), and word of mouth is spreading.

Startup Lessons 28: Know The Best Tools

From wireframing, prototyping, app development, social media, customer support, sales, design, networking, messaging, team building, analytics, emailing, shipping, hosting, legal, accounting, publishing, testing, to promoting and more, there are countless tools that can take a lot of the friction, challenges and hassle out of building and growing a startup.

It is worth spending quality time discovering, evaluating and testing some of the tools that can add value to your startup. The combination of the right tools and existing relevant apps can make startup initiation, idea validation and scalability faster and cheaper.

Startup Lessons 29: Overcome Fear Of Failure

Many dream, far fewer proceed. Failure is doing the things you hate in fear to not do well at the things you love. This all sounds good, but what about disappointments, family to support, mortgage to pay off, retirement to prepare for, kids to educate, etc.? None of this is at stake until your solution proves its value, revenue grows steadily if not exponentially, investors are interested, and talents are willing to work for free. From now until then, no fear justifies delaying execution and taking the necessary steps to build a venture worth committing to.

Startup Lessons 30: Know The Numbers

The best decisions are based or inspired by numbers. No need for a finance or statistics degree, key metrics are loud and clear and can be found and learned easily. Revenue, growth rate, income, margin, customer acquisition cost, churn rate, customer lifetime value, burn rate, runway, break-even point, net promoter score, and bounce rate are some of the most important metrics that every startup founder must know.

Startup Lessons 31: Beware of Behavioral Biases

Most of us are tricked by our own mind. For instance, behavioral research shows that people’s opinions, once formed, tend to stick for too long, a bias referred to as belief perseverance. Furthermore, people tend to seek information that confirms with their existing beliefs; confirmation bias.

Anchoring happens when people form opinions based on the first piece of information they receive and resist to adjust from the initial, possibly arbitrary value they start with. People tend to be overconfident in their judgments and overly optimistic about their abilities. Biases can be difficult to mitigate but must be controlled. Awareness is the first step to realism.

Startup Lessons 32: Creating A Legal Entity Doesn’t Make A Company Out Of Your Idea

Many entrepreneurs believe that one of the prerequisites of starting a startup is to create a legal entity, along with building a product (app) and getting an office space. None of these need to happen until some form (qualitative validation, early traction and/or revenue) of idea validation takes place. Ideas are educated guesses pending proof. Entrepreneurs are better off proving the viability of their solutions before incorporating their startups.

Startup Lessons 33: No One Can Steal Your Idea

Building a successful startup in such a competitive environment is a bumpy journey. Some people may want to hear you over and “steal” your genius but what about execution? The truth and reality is that no one will put in the effort on a consistent basis if it is not something they truly believe in and have spent some time planning and looking forward to.

Furthermore, a research study by Cornell University shows that practical ideas are more valued than unique and creative ones. This is because novel ideas are characterized by uncertainty, challenge and risk. In other words, people feel more lazy executing on innovative ideas. Unless a startup is competing with others over an imminent patent, unique approach or marketing acquisition campaign and things of this sort, entrepreneurs should spend less time worrying about their ideas and more time proving its value through execution.

Startup Lessons 34: Solve Painful Problems And Address Urgent Needs

The bigger the problem, the bigger the business opportunity. Similarly, the more urgent buyer needs are, the more likely they will adopt your solution and pay a premium for it. Keeping in mind this rule of thumb is the best way to evaluate the potential of an idea. In other words, to build a billion-dollar company, solve a billion-dollar problem or one that a hundred million people are willing to pay for.

This is easier said than done but certainly a framework to follow. As of today, Facebook is almost a $760 billion company because it addresses one of human’s most urgent needs; the need to be social according to Maslow’s hierarchy of needs.

Startup Lessons 35: Funding Doesn’t Guarantee Startup Success

Funding is an accelerator and not a success warranty. With funding, you would be able to do things a lot faster a lot sooner with a lot more people. Is this the startup success formula? Not always. Often times, funding is a sign of market potential. It also puts a valuation on the startup. Those are some of the little things that can help pave startup founders towards the right path for an exit.

With funding comes responsibility such as investor expectation, limited decision making, tight deadlines, management responsibility and more. It’s a tradeoff. Striving to build the next disruptive startup, one may believe funding is the only way there. Although it can be an enabler, funding by no means guarantees success. The proof is in the numerous well-funded startups that never survived to see the light of the day.

Startup Lessons 36: Investors Fund Entrepreneurs And Not Ideas

A great team can turn an OK idea into a great idea whereas an OK team may not even execute well on an excellent idea. In other words, investors are more interested in the driver and not us much in the bus or destination. Founders with passion, commitment and attachment to the problem in hand, are more likely to deliver long term results.

There is a lot of weight on ideas too but ideas to some degree are a reflection of entrepreneurs. In sum, while good ideas are necessary ingredients, they are not sufficient to attract investors’ interest. People fund people.

Startup Lessons 37: Revenue Is Not Necessarily The Main Startup Valuation Variable

For early stage pre-revenue startups, valuation is based on benchmarks and a series of educated guesses about the growth potential. A million-dollar valuation on an early-stage startup doesn’t mean a buyer is willing to pay a million dollar for it today. Startup valuation is mainly dependent on the industry, traction, background of the entrepreneur, competing startups, option pool, growth potential and revenue.

To increase valuation, entrepreneurs should worry less about the things they can’t control (competition, industry changes, and competing investors) and focus more on the things they can; team, traction and option pool.

Startup Lessons 38: Startups Are Not Always About Innovation

Often times we tie startups with innovation when it is not always the case. Not every growing and profitable startup is innovative. There are other startup strategies that may not make a big dent in the world but can certainly solve problems and address unmet needs; namely by replicating, repurposing or upgrading existing solutions.

Replication is about taking an existing model and adopting it to a new condition. Repurposing is when existing models are adopted to new solutions, and finally upgrading or enhancing existing solutions through quality, speed and performance is a form of competitive advantage and startups can be built out of this strategy.

Startup Lessons 39: You Can Start Part Time But Can Only Grow Full Time

Startup initiation is more of an attitude than effort. It’s the attitude that drives entrepreneurs to find answers and proof. Ideating, meeting with 100-200 potential users, building a testing version of the product, seeking user input, building again and validating can definitely be done part-time if resources are limited. It sure is a better decision than doing nothing. With traction, revenue and possibly an investment, entrepreneurs can commit to the venture full-time.

Before starting up part-time, know what it will take for you to dive in full-time such as 10 paying customers, 200 active users, $2,000 in monthly revenue, or a $100,000 investment, and finally, grind smart by taking educated steps centered around user needs and not a mission to prove a product no matter what it takes.

Startup Lessons 40: You Don’t Need To Be A Startup Genius To Build One

This is also true for every other field. For instance, you don’t need an accounting degree to be the best at what you do or a science degree to be a scientist or an art degree to be an artist, etc. Though degrees are not a measure of genius, the point is that unlike most fields where a career is dependent on the past performance, building a startup has no high school or collegiate requirement and can be done the moment entrepreneurs decide to.

Learning about startups and best practices also doesn’t require months and years of book readings, conferences, advisement, courses, etc. Instead, founders are better off identifying 3-5 trustworthy sources (books, blogs, lectures, etc.), get equipped with the necessary information and acquire knowledge as startup progress is underway.

Information overload is one of the reasons behind entrepreneurs’ failure to execute on their ideas. It can create confusion, panic, worry and disinterest as every source can approach a topic in a different way making the reader wondering who to follow and what to do.

Startup Lessons 41: You Don’t Need To Be A Programmer Either

You don’t need to be one but you need to know the tools, frameworks, languages and best practices to be of value in every aspect of the startup even if you are not the programmer or technical lead. Understanding technology and where it is heading is how you can propose viable solutions, evaluate team work, and hire the best. This will not make you a programmer but a good leader and decision maker.

Finding complementary skills while focusing on what you do best is what will make a difference in the future. Initially, every technology startup entrepreneur must acquire foundational technical skills.

Startup Lessons 42: Things Never Go As Planned. Be Open For Change

Most startups end up doing something completely different than what they originally intended and that is normal. This fact has little to do with industry knowledge or experience. Stubbornness and attachment to the original plan can be detrimental when the better ideas and directions are not exploited.

Startup founders must be open for change at any point because the we’ve done so much already attitude is likely to disappoint two groups rather one: team and customers.

Startup Lessons 43: Bootstrapping A Startup Doesn’t Mean Spending $0

Bootstrapping is about utilizing existing, self-generated and acquired resources to take an idea or company from one point to the other without referring to investors or banks. Bootstrapping doesn’t make a startup need less resources. Bootstrappers should acknowledge that some investment must be made along the way but must focus on building a self-sustaining solution that can feed itself from generated revenue.

Startup Lessons 44: Perseverance Is A Differentiator

Tens of thousands think about new ideas all the time, a thousand of them take the first steps, a hundred of them resist failure and make extra efforts to move forward, only a few of them make it. Survival signals uniqueness and commitment. In other words, from an investment stand point, reaching the idea pitch day signals entrepreneurs’ competitiveness in passing the thousand others who are fighting for the same reward.

Mere persistence differentiates between dreamers and success stories. Although fewer competing founders doesn’t necessarily guarantee startup success, it ensures survival of the fittest.

Startup Lessons 45: Don’t Be Afraid To Fail. You’re Building Personal Value Regardless Of The Results

Building a successful startup is not given. Thousands attempt, many try hard and only a few make it. If you’re at the hustling stage, consider yourself a winner regardless of whether you are moving in the direction of building the next big thing, deciding to start another startup or completely change careers.

The fact is that building a business, more specifically a startup, is the best educational and professional investment any person can make because they get exposed to every aspect of a business including but not limited to enhancing managerial skills, decision making, learning to work under pressure with limited resources, becoming better negotiators, sales people, content writes, etc.

Entrepreneurs are learning and improving new skills and tools sometimes on a daily basis. Doing this while building startup value is one of the best career development experiences anyone could have. The worst-case scenario is not bad after all. You’re building personal and professional value while turning ideas into reality.

Startup Lessons 46: Do It Because You Really Want To

If there is no will, entrepreneurs are almost literally building to fail. I kind of want to build a startup doesn’t work. It takes effort, disappointment, and a long time to build a very successful company. For this and many other reasons, building a startup for the fun of it will rarely have a happy ending. If the startup is built for learning and/or as a side project, that’s another story.

Furthermore, the most successful startups are built out of a personal need. This is common sense because entrepreneurs would be willing to put in more effort and commitment if it is a problem they deeply care about solving. In sum, the most successful startups are built by those who feel a sense of urgency to solve a problem they and many like them face.

Conclusion

- Technology startup knowledge is no different than general business knowledge in that it is about solving problems using products and services.

- It’s the execution that matters. Knowledge has no value if not used to build startup value.